All Categories

Featured

Table of Contents

I paid into Social Safety for 26 years of significant earnings when I was in the exclusive industry. I do not want to return to function to obtain to 30 years of substantial earnings in order to stay clear of the windfall elimination stipulation reduction.

I am paying every one of my bills currently however will do more traveling once I am gathering Social Safety. Should I wait until 70 to accumulate? I assume I require to live up until regarding 84 to make waiting a great choice. I tried to obtain this response from a financial planner at a cost-free workshop and he would certainly not tell me without employing him for further assessments.

If your Social Safety advantage is absolutely "enjoyable cash," instead than the lifeline it acts as for lots of people, optimizing your advantage may not be your top priority. However get all the information you can about the price and advantages of claiming at various ages before making your choice. Liz Weston, Qualified Financial Coordinator, is a personal finance reporter for Inquiries may be sent to her at 3940 Laurel Canyon Blvd., No.

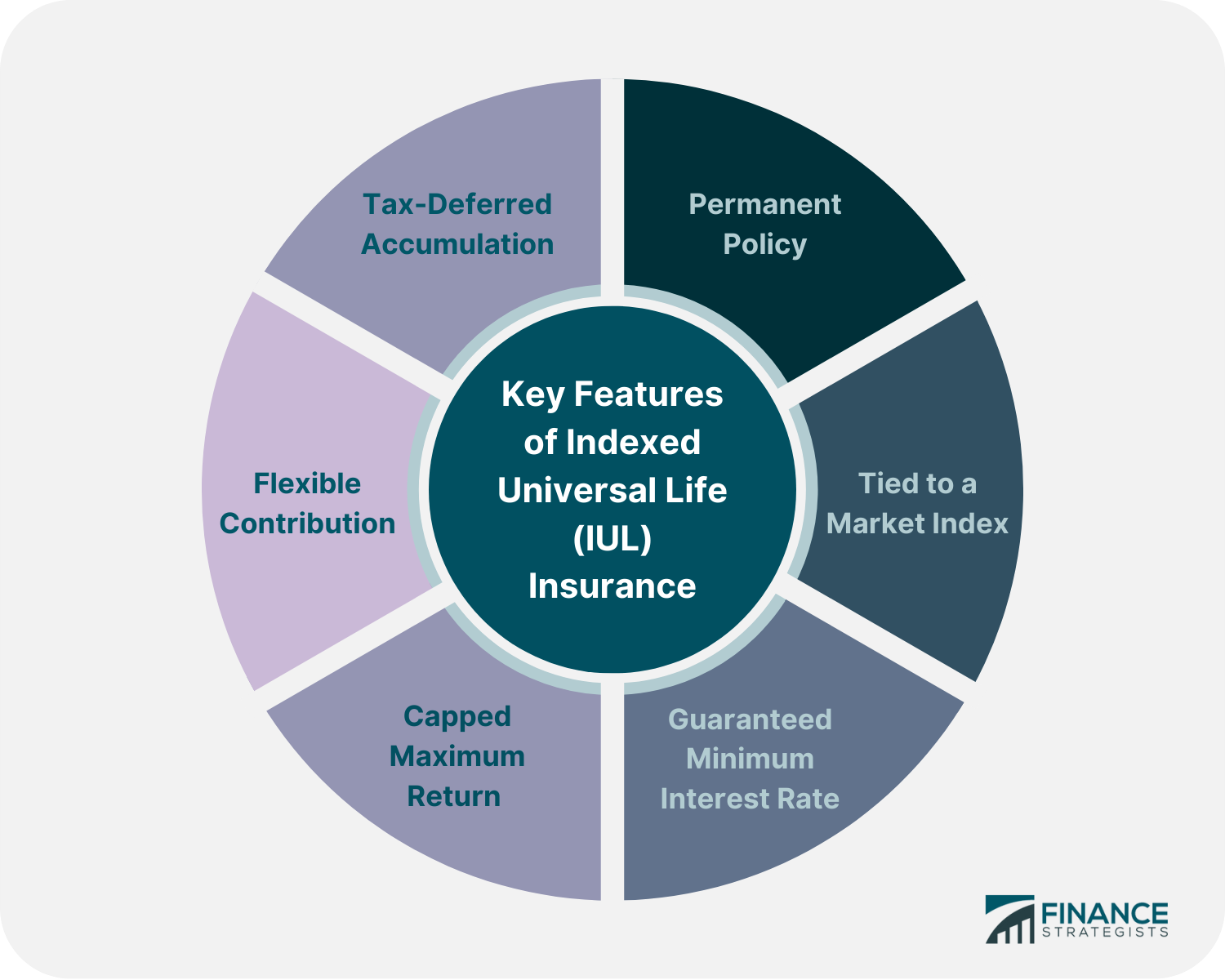

Money worth can accumulate and expand tax-deferred inside of your policy. It's important to note that outstanding plan financings accumulate rate of interest and lower money worth and the fatality advantage.

Nonetheless, if your cash money value falls short to expand, you may need to pay higher premiums to keep the plan effective. Plans may supply various alternatives for expanding your cash money value, so the attributing price depends upon what you pick and just how those choices do. A fixed segment makes interest at a defined price, which may alter with time with economic problems.

Neither type of policy is always better than the various other - everything comes down to your objectives and approach. Entire life policies may interest you if you like predictability. You know exactly just how much you'll require to pay each year, and you can see just how much cash money worth to expect in any given year.

Who Should Buy Universal Life Insurance

When examining life insurance requires, review your long-lasting goals, your existing and future expenses, and your need for safety and security. Discuss your objectives with your agent, and pick the policy that works ideal for you. * As long as needed costs payments are timely made. Indexed Universal Life is not a safety financial investment and is not an investment out there.

Last year the S&P 500 was up 16%, however the IULs growth is capped at 12%. That doesn't seem also bad. 0% floor, 12% potential! Why not?! Well, a pair points. These IULs ignore the presence of returns. They check out simply the modification in share cost of the S&P 500.

Indexed Universal Life Unleashed

Second, this 0%/ 12% video game is basically a shop trick to make it seem like you always win, however you don't. In the last 40 years, the S&P 500 was up 31 years. 21 of those were above 12%, balancing virtually 22%. It turns out missing out on the significant development hurts you way much more than the 0% disadvantage aids.

If you need life insurance, get term, and spend the rest. -Jeremy via Instagram.

Your current browser may restrict that experience. You might be using an old web browser that's in need of support, or setups within your web browser that are not compatible with our site.

Your present internet browser: Discovering ...

You will have to provide certain supply specific yourself regarding your lifestyle in way of living to receive an indexed universal life insurance quoteInsurance coverage Cigarette smokers can expect to pay greater costs for life insurance policy than non-smokers.

What Is Fixed Universal Life Insurance

If the policy you're looking at is generally underwritten, you'll need to complete a medical examination. This test entails conference with a paraprofessional who will certainly get a blood and urine sample from you. Both examples will certainly be checked for feasible wellness threats that might impact the sort of insurance coverage you can get.

Some aspects to consider include the number of dependents you have, the amount of revenues are entering into your household and if you have expenses like a mortgage that you would certainly want life insurance policy to cover in case of your fatality. Indexed universal life insurance is just one of the extra complex sorts of life insurance coverage currently available.

If you're looking for an easy-to-understand life insurance plan, nonetheless, this may not be your best option. Prudential Insurance Firm and Voya Financial are some of the largest service providers of indexed universal life insurance coverage.

Universal Life Insurance Phone Number

On April 2, 2020, "A Critique of Indexed Universal Life" was provided via numerous electrical outlets, consisting of Joe Belth's blog site. (Belth's summary of the original piece can be located below. His follow-up blog site having this short article can be located here.) Not surprisingly, that item produced substantial remarks and criticism.

Some dismissed my remarks as being "persuaded" from my time helping Northwestern Mutual as a home workplace actuary from 1995 to 2005 "regular entire lifer" and "prejudiced against" products such as IUL. There is no contesting that I benefited Northwestern Mutual. I enjoyed my time there; I hold the firm, its staff members, its products, and its common philosophy in prestige; and I'm thankful for all of the lessons I found out while used there.

I am a fee-only insurance expert, and I have a fiduciary commitment to watch out for the finest interests of my clients. By meaning, I do not have a prejudice toward any kind of type of product, and as a matter of fact if I uncover that IUL makes good sense for a client, then I have a responsibility to not just present yet advise that choice.

I always aim to put the finest foot ahead for my clients, which indicates making use of designs that reduce or get rid of compensation to the best level feasible within that particular policy/product. That does not always imply suggesting the plan with the most affordable compensation as insurance is much much more complex than just comparing payment (and often with products like term or Guaranteed Universal Life there merely is no commission versatility).

Some recommended that my level of passion was clouding my judgement. I enjoy the life insurance policy sector or a minimum of what it could and ought to be (universal life insurance rates by age). And indeed, I have an incredible quantity of passion when it concerns hoping that the market does not get yet another black eye with excessively confident images that set consumers up for disappointment or even worse

Ul Mutual Insurance Company

And now history is repeating itself once more with IUL. Over-promise now and under-deliver later. The more things transform, the even more they remain the exact same. I might not be able to transform or conserve the sector from itself with respect to IUL products, and honestly that's not my goal. I wish to help my clients maximize value and prevent critical blunders and there are consumers around every day making inadequate choices with regard to life insurance policy and particularly IUL.

Some individuals misunderstood my objection of IUL as a blanket recommendation of all points non-IUL. This could not be additionally from the reality. I would certainly not directly advise the huge bulk of life insurance policy policies in the market for my customers, and it is unusual to locate an existing UL or WL policy (or proposition) where the presence of a fee-only insurance coverage consultant would certainly not add substantial customer worth.

{kind=link}

Latest Posts

Iul Marketing

What Is The Difference Between Universal And Whole Life Insurance

Pros And Cons Of Indexed Universal Life Insurance